Palladium Still a Better Bet Than Platinum

August 29, 2011

Palladium continues to defy underlying market fundamentals, suggesting it remains sorely undervalued relative to platinum. At less than half the cost of platinum, palladium's absurdly low price is putting more pressure than ever on total global supply. Although nearly as much platinum is mined annually as palladium (only a 7.5% differential, according to USGS data), palladium is in its fifth consecutive year of supply deficit, which widened 500% last year alone, and platinum is expected to enter a seventh consecutive year of surplus.

The recurring supply deficits are partially attributable to substantial declines in annual sales of Russia's state stockpiles, which have long been used to help meet total global demand (and/or suppress market prices). GFMS data suggests that such sales dropped 27% last year, lending some credence to Russian mining giant, Norilsk Nickel's claims that the government stockpiles have been nearly depleted. Russia's state palladium sales will continue through 2012, according to a finance minister, but it's highly doubtful the total will exceed last year's and even more unlikely there will be any sales at all in subsequent years.

Russia's diminishing state stockpiles aren't only to blame. Norilsk, which contributes about 40% of all the world's palladium mine supply, reported a 5% decline in 1H 2011 production to 1.425 M oz. This indicates a possibility that output will be lower for the full year and beyond, as the company has no apparent plans to dramatically increase production in the near future.

Fortunately, other major palladium-producing countries will pick up the slack. South Africa, which also mines roughly 40% of the world's total palladium, is mostly on track to increase total output despite a series of labor disputes and safety stoppages. The third and fourth largest producers, the U.S. (Stillwater Mining Company) and Canada (North American Palladium), have both reported higher output year-to-date.

So, supply should be stable this year; however, it's physical demand that's the real concern. Since both palladium and platinum are used interchangeably in many industrial applications (particularly in the automotive sector), global physical palladium demand is now growing more than twice as fast--and even faster in the world's largest automobile markets. Chinese palladium demand, for instance, increased nearly 46% last year alone, compared to an 8% drop in platinum demand. The country's burgeoning automotive sector may have slowed somewhat in the first half, but recently published figures for June and July show a significant turnaround following the Chinese government's launch of a "Cash for Clunkers" type of program. Auto manufacturing in China is up about 2.5% so far and it's quite likely the country's palladium imports will surpass last year's total.

Indian auto sales surged 30% in 2010, albeit at a slightly slower pace, and production (yr/yr) has grown by double digit percentages every month this year. Similarly, auto sales in Brazil climbed 10% during the first half to a record high. Production seems to be keeping pace and could continue as China's JAC motors, Japan's Suzuki and S. Korea's Hyundai are all planning to launch new manufacturing operations in Brazil. These trends suggest palladium imports to both India and Brazil will be higher by year's end.

The U.S.' auto industry may have been severely impacted by the Japanese earthquake in March, but palladium imports were still up during the first half with a noticeable 60% yr/yr increase in June, according to preliminary U.S. Dept. of Commerce statistics.

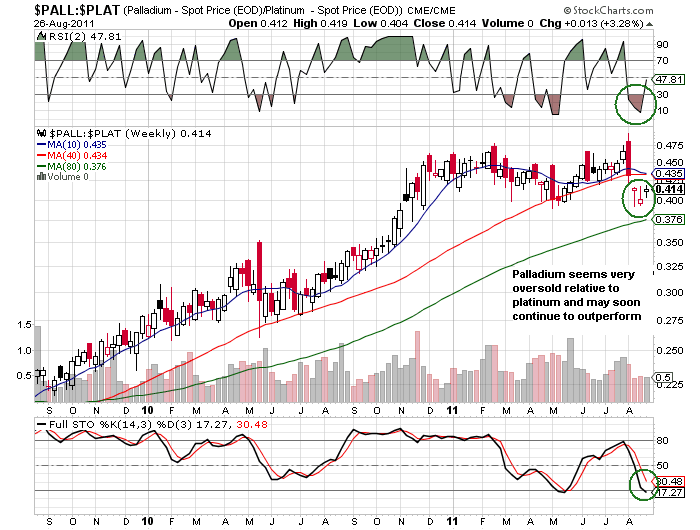

As long as palladium prices remain far cheaper than platinum, we could continue to see deeper palladium supply deficits and growing platinum surpluses (at least in the short term). Because demand for palladium will continue outpacing supply, there's little doubt that prices will at least reach parity with platinum in the years ahead.

This article was originally published by Investinations on www.argmaur.com.